Real Assets Investing Primer

Real assets have become one of the cornerstones of many investment portfolios, offering investors the potential opportunity to access physical, durable assets that mainly derive value from their utility and scarcity. These assets may provide diversification relative to traditional equities and fixed income, maydeliver relatively stable income streams, and possess inflation hedging characteristics related to the ability to reset rents as leases expire. 1 Among the most adopted strategies within real assets are real estate, infrastructure, farmland, and timberland. This paper is designed to serve as a primer on each of these asset classes, highlighting their key characteristics and relevance for investors.

Real Estate

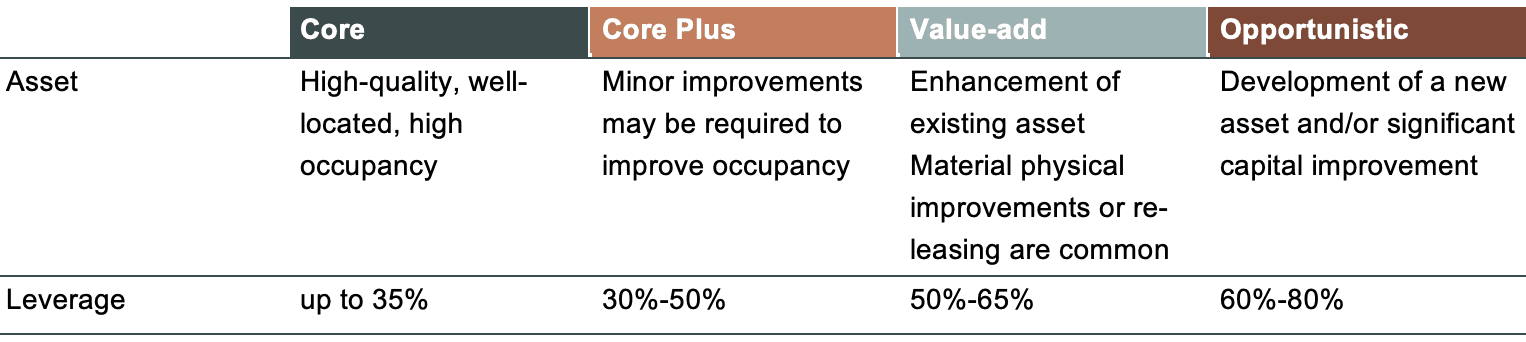

Real estate is the most established of the real assets strategies and involves ownership ofphysical properties. Property sectors include residential, office, retail, industrial, and hotels, and alternatives such as data centers, senior housing, student housing, medical offices, self-storage, and life sciences. Returns are typically produced by a combination of rental income and appreciation in property values. Strategies are generally organized by relative risk, commonly measured by leverage, and return.

Real estate may be an attractive investment due its potential to generate both current income and long-term capital appreciation. Long-term leases may stabilize cash flow, while replacement costs and rents tend to move with inflation. Callan’s analysis of historical correlation of performance across asset classes shows that private real estate has historically exhibited generally low correlation with public equities and bonds, potentially improving portfolio efficiency by lowering volatility and enhancing diversification within multi-asset portfolios. 2 The asset class may also provide durable income streams, potential for capital appreciation, and positive inflation sensitivity. However, it's important to note that distributions and returns are never guaranteed and that these investments carry a high degree of risk, including the risk of total loss of capital. Past performance is no guarantee of future results or success.

Performance is further shaped by supply and demand fundamentals. Demand typically reflects macroeconomic growth, labor market conditions, demographic shifts, and sector-specific drivers such as e-commerce adoption and hybrid work. On the supply side, development activity may be influenced by land availability, regulatory approvals, construction costs, and the availability of financing. Callan has observed that periods of low supply and high demand have generally resulted in strong rent growth and asset value appreciation.

Infrastructure

Infrastructure refers to the integrated systems that enable the movement of people, goods, energy, and information. Sectors include transportation, energy and power, digital infrastructure, utilities and environmental, and social infrastructure (which includes hospitals and schools). Infrastructure’s value is primarily derived from its essential nature: airports, toll roads, power plants, fiber networks, and water treatment facilities are all foundational assets on which economies depend. Unlike real estate, infrastructure is typically less tied to the business cycle, given the inelastic demand and the monopolistic or duopolistic market structures in which many of these assets operate. Infrastructure investment opportunities are often distinguished as greenfield or brownfield:

Greenfield: New infrastructure developed from the ground up

Brownfield: Existing, operational assets generating established cash flows

Infrastructure investing may provide long-term cash flows, while offering diversification and potential resilience across market cycles. Some projects also include contractual rent increases linked to inflation, potentially making the asset class a hedge. Like real estate, investors classify strategies across a risk/return spectrum: core, core-plus, value-add, and opportunistic. Risks include political/regulatory intervention, permitting and construction delays, counterparty credit quality, and commodity price sensitivity in energy-linked sectors.

Infrastructure demand is typically driven by factors such as population growth, urbanization, digitalization, and the global transition to low-carbon energy. On the supply side, new development is generally constrained by high capital requirements, long lead times, and regulatory complexities. Callan has observed that this combination of generally resilient demand and limited new capacity has historically supported relatively stable cash flows.

Farmland

Farmland investing entails the acquisition and management of agricultural land for crop or livestock production. Investors may lease land to operators in an effort to secure a steady income stream, or manage farms directly with the goal of capturing both operating profits and appreciation. Farmland may be attractive because it can provide consistent annual cash yields. There are two primary types of farmland investments:

Row Crops: Annual crops such as corn, wheat, rice, and soybeans that are replanted each season. They generally are perceived by the market as lower risk compared to permanent cropsbecause farmers can adjust in the event of inclement weather, drought, or other circumstances. Theymayalso have a lower commodity risk because farmers can change the crop the next year if demand and pricing lag.

Permanent Crops: Long-lived crops such as orchards and vineyards that produce income over decades. Permanent crops generally exhibit a J-curve effect, with low yields early on and rising income as plants mature.

Farmland combines potential for yield with long-term appreciation and provides exposure to themes like food security and sustainable agriculture. Historically family-owned, farmland has been increasingly sold to institutional investors as many retiring farmers lack successors[Global Ag Investing, January 2018]. The asset class offers diversification from equities and bonds, inflation protection given the link between food prices and consumer inflation, and land values that have proven resilient across cycles[National Council of Real Estate Investment Fiduciaries (NCREIF), September 2025].

According to Callan’s discussions with farmland investment managers, demand for farmland is being driven higher by population growth, rising protein consumption, and the expansion of markets such as biofuels. On the supply side, farmland investment managers share that availability is generally constrained by urbanization, soil degradation, and limited arable land. Technology and precision agriculture are helping to improve yields, though risks such as climate and weather volatility, commodity cycles, trade and policy shocks, tenant execution, and water scarcity remain significant.

Timberland

Timberland investing involves the ownership and management of forests for the purpose of generating financial returns. What makes timberland distinctive is its biological growth component: trees grow in volume and value regardless of broader economic cycles. Investors have the option to harvest when market conditions are favorable or to defer cutting, effectively storing value “on the stump.” This feature provides a form of natural optionality and may help to smooth return volatility over time.

Timberland often offers modest yield, long-term appreciation, and natural inflation sensitivity, supported by the biological growth of trees and flexibility in harvest timing. Beyond timber revenues, investors may access alternative income through carbon sequestration, biodiversity credits, and conservation agreements, which may add diversification and upside potential.

Demand is typically anchored in construction and packaging markets, with housing activity as a primary driver, while supply is limited by conservation policies and restricted land conversion. However, despite its favorable attributes, timberland has historically underperformed its real assets counterparts on a total-return basis [NCREIF, September 2025]. Risks such as wildfire, pests, disease (exacerbated by climate change), and exposure to cyclical housing markets remain important considerations. While timberland can serve as a diversifying and environmentally significant allocation, its role in portfolios may be best viewed as complementary rather than dominant.

Conclusion

Real estate, infrastructure, farmland, and timberland each occupy a distinctive place across the real assets spectrum. Their common appeal typically lies in their tangibility, potential for income and inflation protection, and diversification benefits relative to traditional asset classes. Over time, Callan has observed these asset classes transition from niche allocations to core components of many investment portfolios. Looking forward, we expect that global megatrends—urbanization, demographic growth, technological change, and the transition to a low-carbon economy—will continue to shape their evolution. For investors seeking relatively resilient assets with the potential for long-term value creation, real assets remain a unique and growing part of the investable universe.

Return Metrics

Because real assets strategies may be offered through both perpetual-life vehicles (e.g., open-ended funds) and drawdown vehicles (e.g., closed-ended funds), the way performance is measured depends on the structure. For perpetual-life vehicles, time-weighted returns are the primary metric. For drawdown vehicles, where the GP controls the pace and timing of capital calls and distributions, performance is evaluated more like private equity or private credit, with an emphasis on IRR, total value to paid-in capital (TVPI), and distributions to paid-in capital (DPI).

TWR: Time-Weighted Return. Compound rate of growth of $1 invested in a strategy over a given period, removing the impact of external cash flows (contributions and withdrawals). TWR isolates the manager’s investment performance by breaking the track record into subperiods defined by cash flows, calculating the return in each subperiod, and then linking those subperiod returns geometrically.

IRR: Internal Rate of Return. The implied discount rate that equates the present value of cash outflows (Paid-In Capital) with the present value of cash inflows (Distributions + NAV). Unlike the TVPI, this calculation incorporates the time value of money.

DPI: Distributions to Paid-In Capital. The portion of TVPI that has been realized as cash is returned to investors.

TVPI: Total Value to Paid-In Capital. A more simplistic ratio that measures the value of a private credit fund (both realized and unrealized) relative to the amount contributed (e.g., a 1.25x TVPI means $1 invested is worth $1.25). Because it does not account for the time value of money, the TVPI is best considered alongside the IRR.