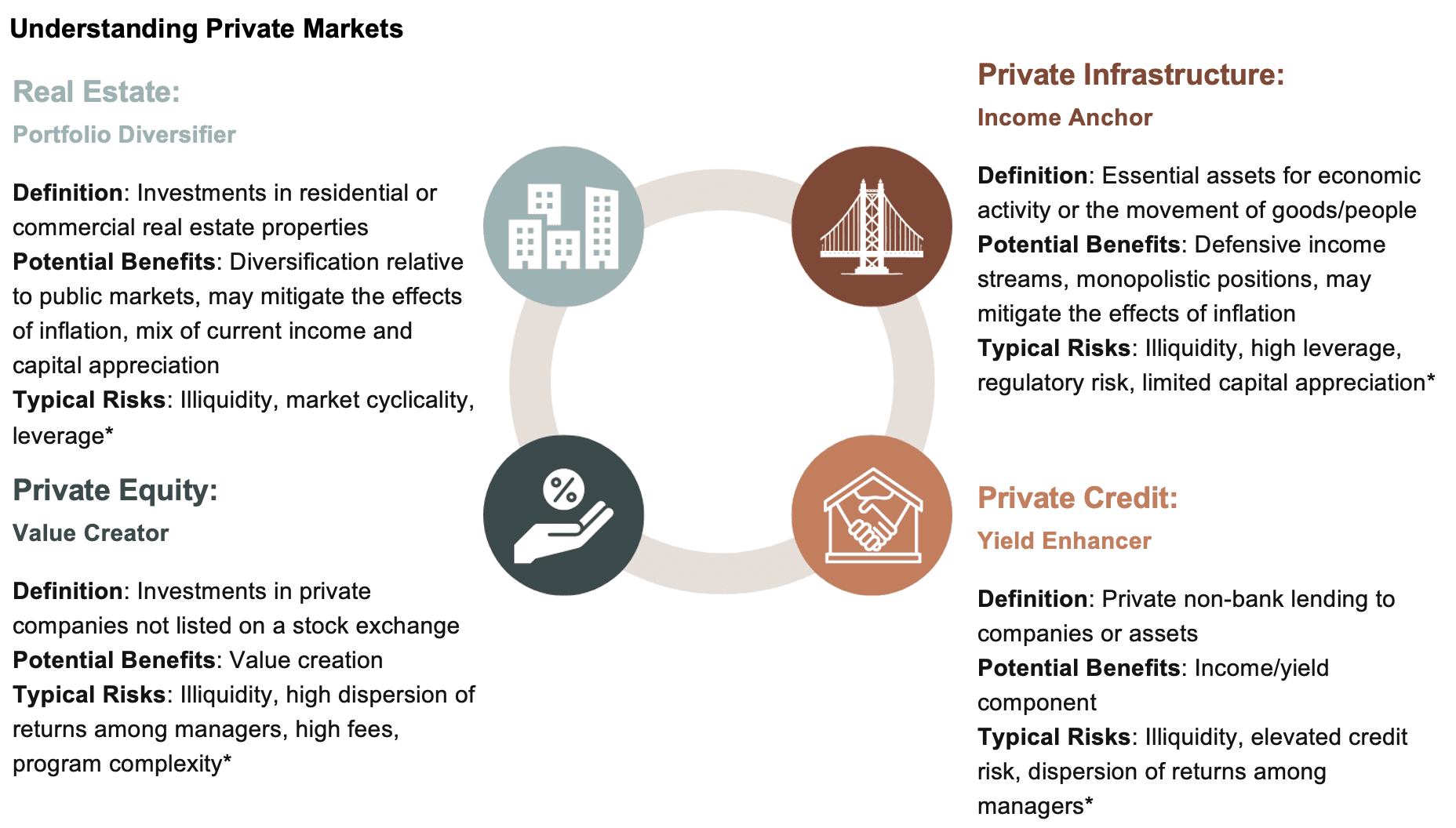

Alternative investments can play an important role in a portfolio, with each asset class offering distinct benefits and risks. Strategies such as real estate, private infrastructure, private equity, and private credit may offer access to differentiated return drivers, potential income generation, and exposure to assets that may behave differently across economic cycles. At the same time, investors should keep in mind the risks associated with these asset classes, namely illiquidity, complexity, higher fees, and valuation uncertainty. As investors explore alternatives, it is important to understand how each strategy functions individually.

Considering each alternative asset class’s risk characteristics, thoughtful diversification across these strategies may help reduce reliance on any single driver of performance. When combined, alternative investments can offer complementary exposures. For example, private infrastructure often emphasizes essential-service assets that can provide the potential for inflation-linked cash flows, potentially making it more defensive during economic slowdowns. Examples could include water and wastewater systems, renewable power assets with long-term contracts, or social infrastructure assets (such as schools, hospitals, and government facilities where revenue is not tied to usage). Meanwhile, Private equity investors typically target return in the forms of long-term value creation and growth of capital, while allocators to private credit seek to realize return primarily through income (interest payments and potentially origination fees), acknowledging that principal (especially in more stressed or distressed credit investments) may be at risk. Together, these strategies can potentially help form a portfolio that aligns with an investor’s unique investment objectives and risk tolerances.

*This is not an exhaustive list of all of the risks that could impact an investor.

Expectations

The benefits and risks of diversifying across private markets asset classes may be best understood by understanding their return and risk characteristics over a typical full market cycle. Some asset classes are designed with the goal of providing steady income, while others aim for higher long-term growth, often at the expense of more ups and downs.

Real Estate seeks to deliver returns through a mixture of income and capital appreciation. With some variability by property type, core real estate (well-leased properties) may offer a relatively stable profile compared to other real estate types seeking to generate returns by way of income. Value-add and opportunistic real estate (properties requiring renovation or new developments) carries significant risk, with a higher risk profile, increased leverage, and greater reliance on capital appreciation.

Private Infrastructure may be underpinned by longer-term contractual income. These assets (utilities, transportation, or energy systems) are typically essential services, which may ensure relatively steady demand and the possibility of more reliable cash flows. If the contracts are also tied to inflation, the asset class may help mitigate the effects of inflation. Taken together, these characteristics may make private infrastructure less impacted by economic shocks.

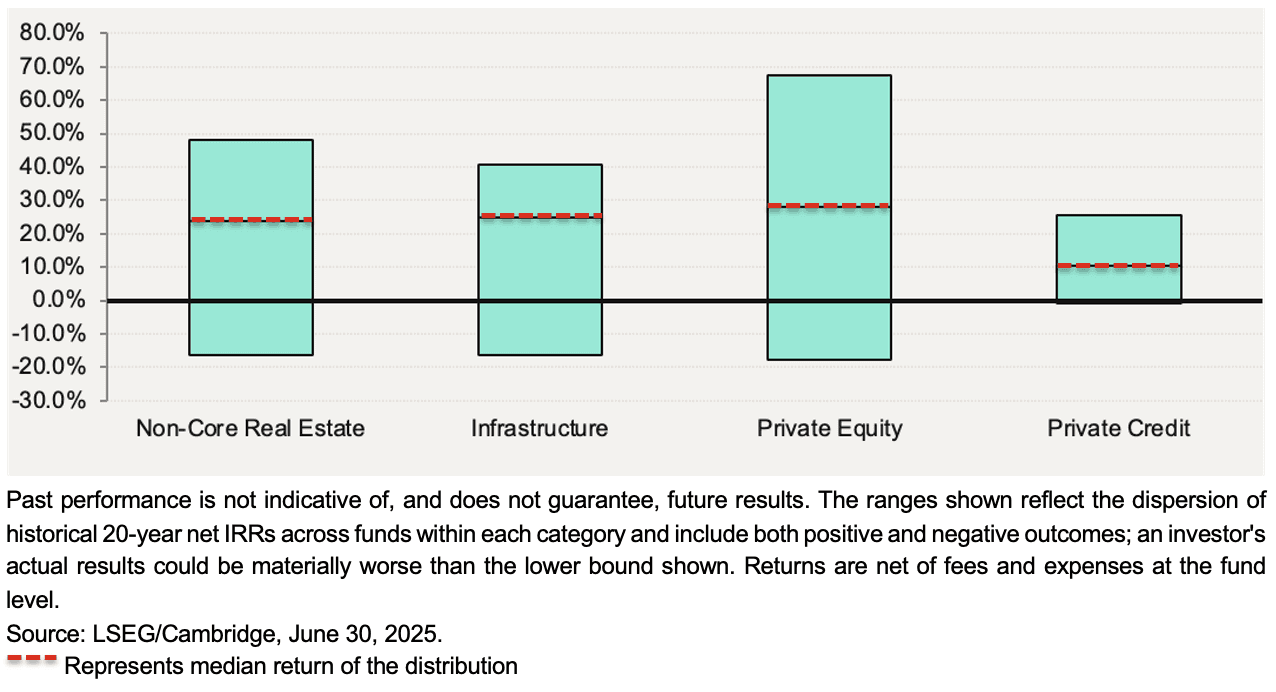

Private Equity sits at the furthest end of the risk and return spectrum, with the highest dispersion of returns amongst managers (LSEG/Cambridge, June 2025). As a result, manager selection can be critical to success. Within the asset class, venture capital (investments in startup businesses) typically poses more risk than other categories, such as buyouts, which usually back more mature companies.

Private Credit typically sits in between real estate and private equity in terms of risk level. Private loans may provide income and may potentially benefit from floating interest rates. While generally carrying less risk than private equity investments, private credit can be vulnerable to credit cycles, particularly when defaults rise as the combination of missed or delayed coupon payments and/or markdowns on the principal of such loans may present a direct hit to the total return of such investments.

Historical Dispersion of Returns by Asset Class

20-Year Net IRRs as of June 30, 2025

Implementation Options

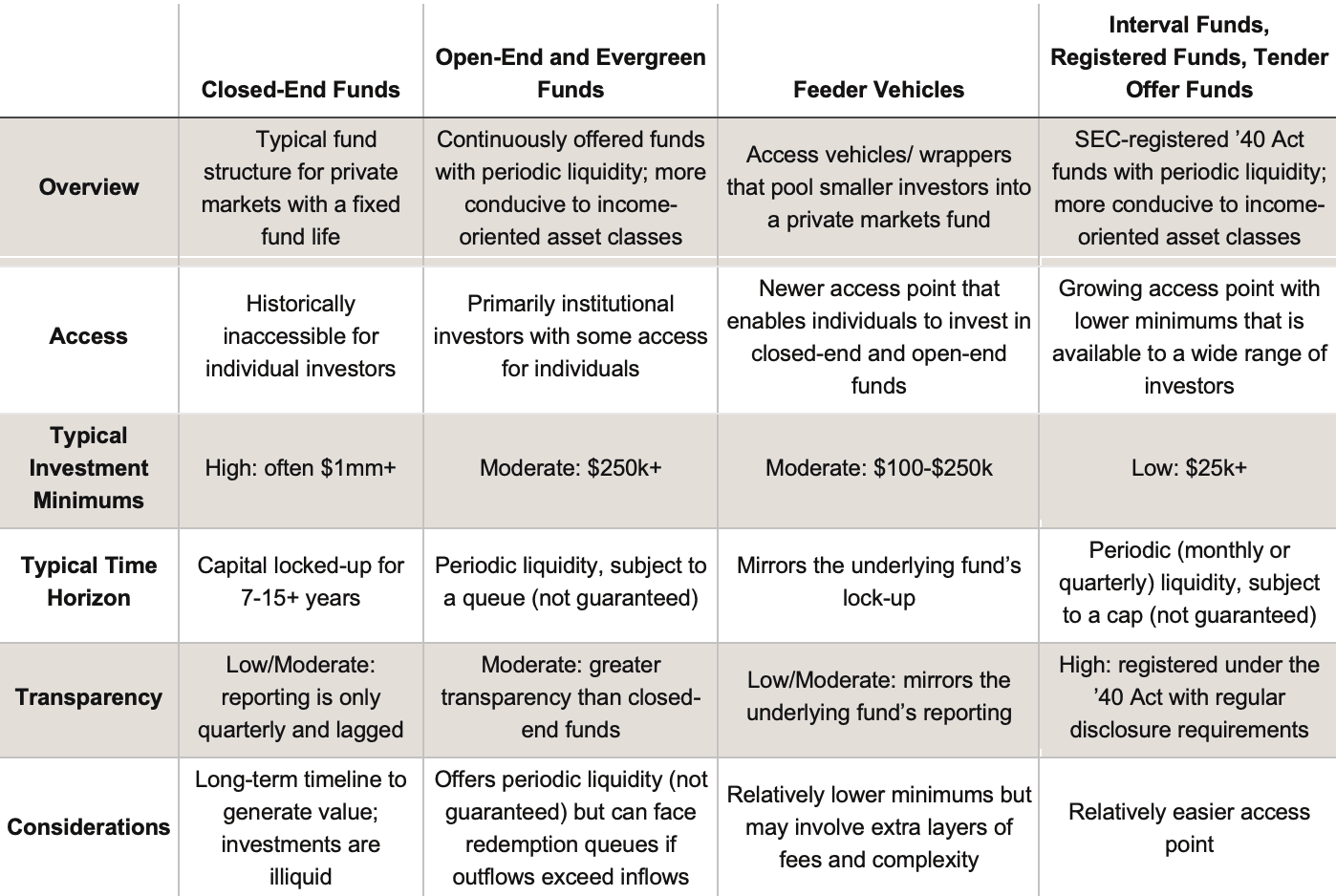

The private markets are becoming increasingly accessible to individual investors. As investors seek to broaden their exposure across private markets, investing through a fund structure may be a path forward, allowing them to pool capital and access a relatively more diversified portfolio. These funds can take different forms, with each asset class offering its own unique structure.

Closed-end funds and open-end funds have served as the traditional access point for private markets, but historically they have been limited to institutional investors. These fund structures typically require high investment minimums—that is, until the advent of feeder vehicles. These vehicles offer a newer access point to similar strategies by pooling the commitments of smaller investors, including individuals.^1^ Outside of closed-end funds, SEC-registered ’40 Act funds (for example registered funds, interval funds, and tender offer funds) represent another rapidly-growing access point for private markets, typically offering lower minimums and periodic liquidity.

Across each category, investors should consider liquidity needs, minimum commitment amounts, return profile, and transparency. Thoughtful portfolio construction should consider the structure of the vehicle as it relates to the investor’s broader objectives, tax considerations, and tolerance for illiquidity. All investors should consider their individual factors in consultation with a professional advisor of their choosing when deciding if an investment is appropriate.

Portfolio Construction Examples

With an understanding of some of the benefits and drawbacks of each asset class, investors should understand how these strategies fit together in a portfolio. There are multiple ways to allocate capital across private markets, each with varying risk and return characteristics. The right mix will vary for investors and depends on the investor's goals and objectives. In addition to helping to reduce concentration risk, prudent diversification can help mitigate cyclicality as asset classes respond differently to economic cycles. A diversified portfolio may also broaden the investor’s opportunity set, providing access to multiple sources of possible growth and yield. By blending these various asset classes, investors may construct portfolios that work to capture various objectives, such as growth potential, while also seeking to provide other characteristics like income generation or downside protection.

If an investor were to construct a portfolio that mirrors the private markets universe (in terms of AUM), the portfolio may look similar to the pie chart below. Increasing or decreasing exposures to each of these asset classes can have cascading effects on the overall profile.

Private Markets Universe

This chart is for illustrative purposes only.

Source: PitchBook, Private Markets AUM (NAV + Unfunded Commitments) as of 2Q’25.

Conclusion

A well-constructed portfolio across real estate, private infrastructure, private equity, and private credit may allow for a potentially diversified combination of growth, income, mitigated effects of inflation, and diversification. Vehicle selection, liquidity trade-offs, and tax implications should be considered in building such portfolios. Ultimately, investors today should view alternatives not as a single-sector bet, but as a diverse opportunity set capable of enhancing their long-term investment outcomes.

Callan is an independent investment consulting firm retained by Crowd Street for various services.