Private Real Estate Debt Primer

Private real estate debt may be a part of a diversified portfolio; it allows diversification from a traditional stock and bond portfolio as well as equity real estate. Investors in private real estate debt act as “the bank” by providing loans to properties. Real estate debt differs from equity in that debt takes precedence in potential distributions,* including income and return of capital. Real estate debt typically is collateralized, with loans secured by the underlying asset. Debt holders potentially can take control of and sell a property to repay themselves if the borrower defaults. *Distributions are not guaranteed.

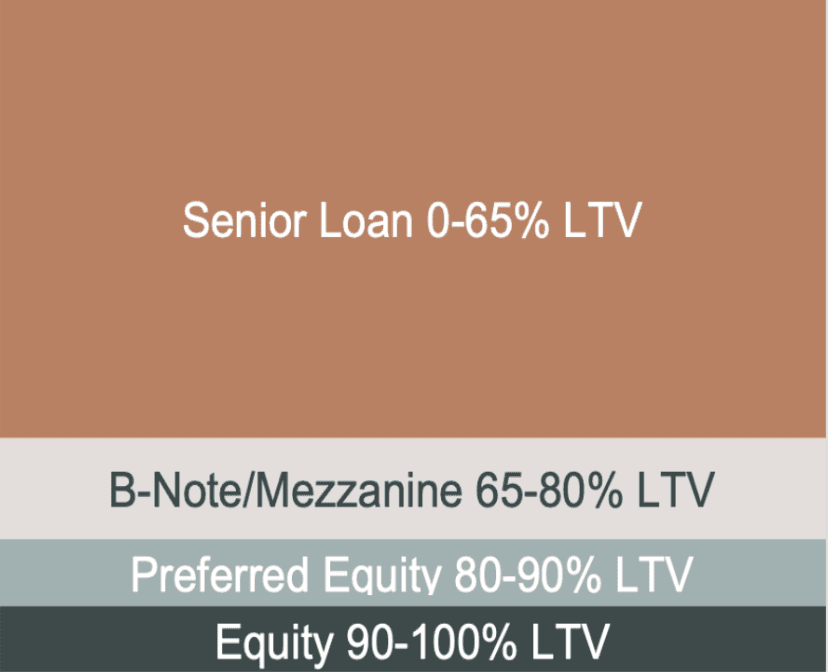

Private Real Estate Debt: What it is and how it stacks up

Real estate debt generally includes loans secured by commercial properties across sectors such as industrial, multi-family, office, retail, hospitality, and alternatives like self-storage, life sciences, and single-family rentals. Yields on real estate debt generally come in two primary forms. Fixed rate loans are typically secured by stabilized properties and generally longer in term (~7-10 years). The rate of interest remains the same for the entire length of the loan. Floating rate loans are typically secured by transitional properties and have shorter terms (2-5 years). Pricing is generally based on a spread over SOFR (Secured Overnight Financing Rate), and the interest rate fluctuates over the term of the loan.

Private real estate debt has many forms. Debt investments can be made in different positions of the capital structure with each position (e.g. senior, junior, mezzanine) having distinct characteristics and rights. Debt structures are typically differentiated by their priority of payment, which relates to their relative risks and can range from debt-like to more equity-like. The variety of commercial real estate debt structures and positions in the capital stack are summarized below. Lenders can originate or invest in different points in the capital stack depending on potential target performance. Key underwriting considerations include loan-to-value (LTV) or loan-to-cost (LTC) ratios, coverage metrics such as debt-service-coverage ratio (DSCR) and debt yield, as well as structural protections like cash traps (restrictions on borrower cash flow), reserves, and sponsor quality.

Senior Loan/A-Note: This is a debt instrument collateralized by a first mortgage or deed of trust that encumbers an income-producing property. The loan is typically the senior-most position in the capital stack and receives a priority claim for interest income and repayment proceeds. Prepayment risk is typically reduced by make-whole covenants that require the borrower to pay a minimum required amount to the lender for loans that are repaid early. The position in the capital stack is typically 50% to 65%.

B-Note: This is a debt instrument that is created by originating a whole loan and selling a senior interest in that loan, with the B-note holding a less-senior position in the capital stack. A B-note typically receives an enhanced return by selling the A-note at a lower yield. The primary source of income for B-notes is rent paid by tenants that occupy the property; however, the A-note holder receives income first. A B-note is generally not terminated through foreclosure and can often participate in liquidation proceeds after more senior positions have received payments in full. A holder of a B-note generally does not have the right to independently exercise remedies. The position in the capital stack typically starts at 50% to 65% LTV and goes up to 75% to 80% LTV.

Mezzanine Loan: This is a debt instrument typically collateralized by a pledge of ownership interest in a property. The mezzanine loan holds a relatively junior position in the capital stack and typically finances a transitional commercial real estate property that needs additional leasing to stabilization and capital upgrades and perhaps a repositioning. The mezzanine lender can execute an expedited foreclosure of ownership interests and gain full control of an asset from a borrower, when in default, if the senior loan is made current by the mezzanine lender. If the senior lender is not being paid, then that lender can foreclose and terminate the mezzanine lender’s interest. The loan structure attempts to minimize the risk to lenders. Senior debt providers primarily prefer A-notes that have subordinate debt in the form of mezzanine loans versus B-notes because a B-note is still part of the first mortgage, which may increase mortgage leverage, probability of default, and capital charges. The position in the capital stack typically starts at 50% to 65% LTV and goes up to 75% to 80% LTV.

Preferred Equity: Investments are made as preferred contributions through an agreement between the property owner and the preferred equity investor with transaction-specific terms and conditions. Investors are typically paid a preferred return after debt providers and before equity investors receive potential distributions. Foreclosure by any secured debt tranches will generally terminate the preferred equity interests. The position in the capital stack typically starts at 75% to 80% LTV and goes up to 90% LTV.

Potential Role Within Diversified Portfolios

Private real estate debt may offer the following features which can be of varying interest to investors:

Income, primarily from property cash flows.

Downside protection compared to real estate equity.

Broad range of investment opportunities.

It has performed well compared to other fixed income options.

Floating-rate loans for well-positioned, well-located investments may offer some interest-rate protection.

Allocations are generally housed within Real Estate, Private Credit, or Fixed Income portfolios. Fund structures range from open-end core/core plus vehicles to closed-end non-core vehicles with relatively higher risk profiles.

Return Metrics

Because Real Estate Debt strategies may be offered through both perpetual-life vehicles (e.g., open-ended funds) and drawdown vehicles (e.g., closed-ended funds), the way performance is measured depends on the structure. For perpetual-life vehicles, time-weighted returns are generally the primary metric. For drawdown vehicles, where the GP controls the pace and timing of capital calls and distributions, performance is generally evaluated more like private equity or private credit, with an emphasis on IRR, total value to paid-in capital (TVPI), and distributions to paid-in capital (DPI).

TWR: Time-Weighted Return. Compound rate of growth of $1 invested in a strategy over a given period, removing the impact of external cash flows (contributions and withdrawals). TWR isolates the manager’s investment performance by breaking the track record into subperiods defined by cash flows, calculating the return in each subperiod, and then linking those subperiod returns geometrically.

IRR: Internal Rate of Return. The implied discount rate that equates the present value of cash outflows (Paid-In Capital) with the present value of cash inflows (Distributions + NAV). Unlike the TVPI, this calculation incorporates the time value of money.

DPI: Distributions to Paid-In Capital. The portion of TVPI that has been realized as cash is returned to investors.

TVPI: Total Value to Paid-In Capital. A more simplistic ratio that measures the value of a private credit fund (both realized and unrealized) relative to the amount contributed (e.g., a 1.25x TVPI means $1 invested is worth $1.25). Because it does not account for the time value of money, the TVPI is best considered alongside the IRR.