Private Credit Primer

Introduction: Private credit has become an increasingly important component of many institutional portfolios, offering investors the potential opportunity to access privately negotiated debt investments that provide financing to non-public companies. These investments may offer relatively attractive risk-adjusted returns, portfolio diversification relative to traditional equities and fixed income, and the potential for income through interest payments. In addition, private credit has historically demonstrated resilience across various market cycles and can serve as a valuable source of capital in periods when traditional lending markets tighten.^1^ Among the most common strategies within private credit are direct lending, distressed debt, mezzanine financing, and special situations. This paper is designed to serve as a primer on these strategies, highlighting their key characteristics and relevance for investors.

Private Credit Defined: Direct lending or other forms of non-bank financing provided to companies outside of the traditional public debt markets. Private credit has grown significantly since the Global Financial Crisis, as banks retreated from middle market lending and institutional investors sought yield in a low-rate environment.^2^

Fund Structure: Private credit funds can be structured as closed-end limited partnerships (typical lifespan of 7–10 years) or as evergreen, open-ended structures. Investors, or Limited Partners (LPs), commit capital that the investment manager, or General Partner (GP), deploys into a typically diversified set of loans and credit instruments.

Why Invest in Private Credit?

Returns: Over a full credit cycle, private credit has historically delivered returns in the 7–12% range, depending on strategy.^3^ The return premium, also known as the “illiquidity premium,” compensates investors for locking up capital and bearing credit risk.^4^

Diversification: May provide portfolio diversification relative to public equities and bonds, with return drivers typically linked to private lending dynamics and contractual income streams. However, it's important to remember diversification does not guarantee investment returns and does not eliminate risk of loss.

Income Generation: Yields are typically higher than broadly syndicated loans or public bonds,^5^ with floating-rate structures that may offer protection in rising rate environments. A floating rate is an interest rate that changes over time, usually based on a benchmark like the prime rate or LIBOR. It moves up or down as market rates change.

Challenges

Illiquidity: Unlike public bonds, private loans are generally illiquid. The secondary market is smaller and more thinly traded. Evergreen or semi-liquid strategies provide more frequent subscription opportunities, typically monthly, and redemption opportunities, typically quarterly.

Fees: Management fees typically range from 0.75%–1.5% with carried interest of 0–15% on profits.

Credit Risk: Borrowers are often middle-market companies with limited access to public capital markets, making credit underwriting and monitoring essential.

Manager Selection: Wide dispersion of performance across managers due to differences in sourcing networks, underwriting standards, and restructuring experience.

Program Complexity: Private credit requires oversight of loan servicing, covenants, and compliance.

Benchmarking: Private credit lacks a perfect benchmark, as no passive, investable index exists. Investors often use a peer group of comparable funds such as the Cambridge Private Credit Index or a public market index with a spread, such as the Morningstar LSTA US Leveraged Loan Index.

Investment Timeline

Investment Period: The GP typically draws capital to originate or purchase loans and credit investments across 20–50+ borrowers.

Income & Amortization: Cash flows typically begin during the first year, as interest and amortization payments are made throughout the loan term. Cash flows can be recycled to make new investments.

Exit / Repayment: Loans typically mature, are restructured, or sold within 2–5 years. Managers can recycle or distribute capital back to investors, depending on fund structure.

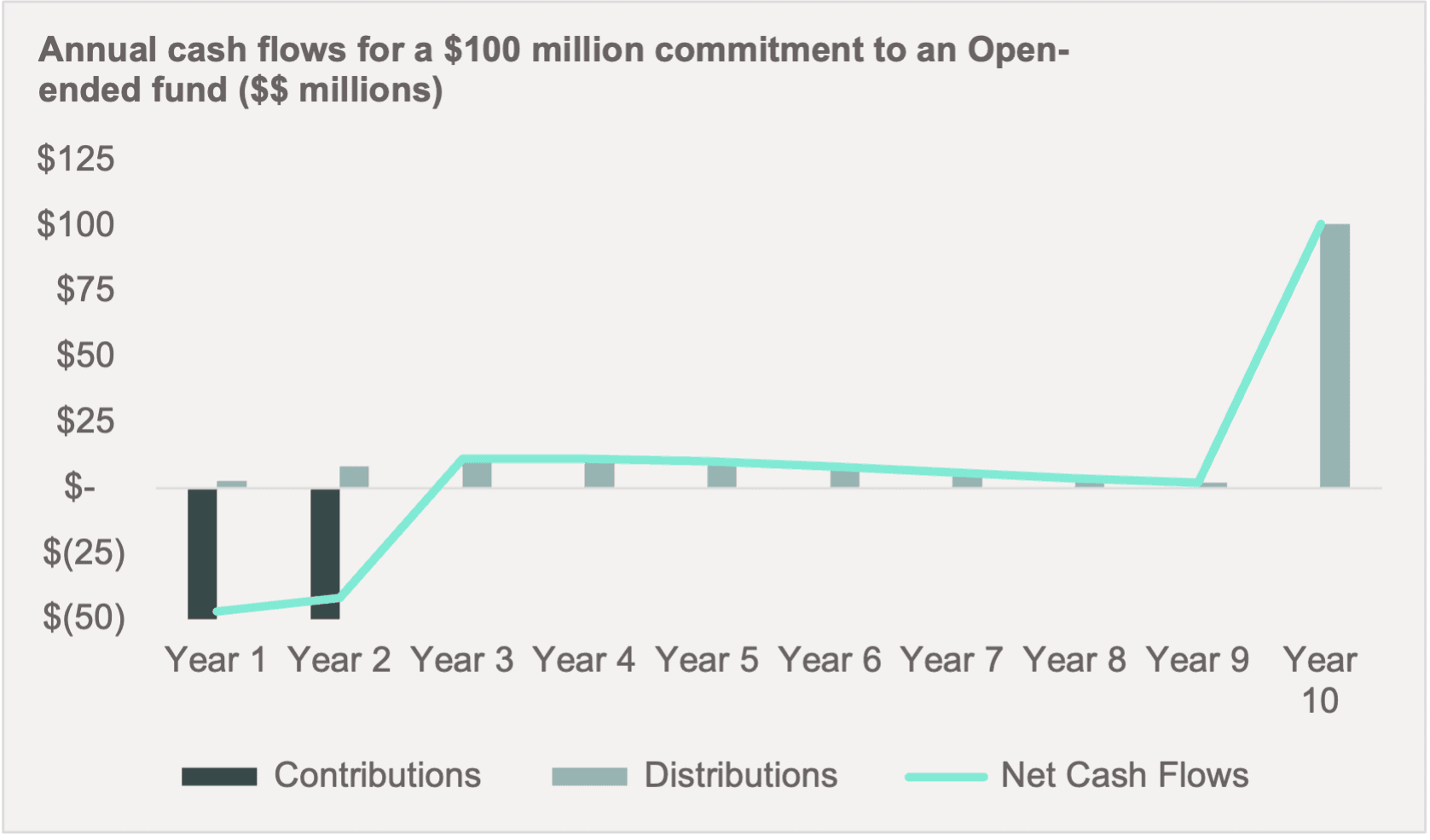

Source: Callan analysis. Note: Data hypothetically illustrates that the LP redeems its principal in Year 10. This chart is for illustrative purpose only. This does not represent an actual investment. Actual results will vary and distributions are never guaranteed.

Strategy Types

Private credit spans a range of strategies, including:

Direct Lending: Senior secured loans to sponsor-backed middle-market companies.

Asset Based Lending/Specialty Finance: Lending against real assets or liquidating pools of non-corporate assets.

Mezzanine Debt: Subordinated loans generally with higher yields, often including equity warrants.

Distressed Debt: Investments in distressed companies, with opportunities for restructuring or control.

Opportunistic Credit: Flexible approach targeting dislocations across credit markets.

Secondaries: Purchases of existing private credit fund interests or portfolios.

Co-Investments: Direct loan participation alongside the general partner, either individually or through a pooled fund.

Return Metrics

Because the GP has discretion over the timing of cash flows, private credit returns generally use the internal rate of return (IRR), current yield, and distributions to paid-in capital (DPI) calculations, rather than the time-weighted returns (TWRs) associated with public equity.

IRR: Internal Rate of Return. The implied discount rate that equates the present value of cash outflows (Paid-In Capital) with the present value of cash inflows (Distributions + NAV). Unlike the TVPI, this calculation incorporates the time value of money.

Current Yield: Annualized interest income as a percentage of invested capital, an important metric for income-focused investors.

TVPI: Total Value to Paid-In Capital. A more simplistic ratio that measures the value of a private credit fund (both realized and unrealized) relative to the amount contributed (e.g., a 1.25x TVPI means $1 invested is worth $1.25). Because it does not account for the time value of money, the TVPI generally is best considered alongside the IRR.

DPI: Distributions to Paid-In Capital. The portion of TVPI that has been realized as cash is returned to investors.