Crowd Street will periodically publish outlooks on the commercial real estate (CRE) market, providing a high-level overview of some macro trends, sector and regional performance, and key themes we’re seeing in active deals.

It’s designed to complement the more frequent, in-depth CRE insights published to the website.

I. Introduction: Has CRE Found Its Footing?

Macroeconomic and regulatory uncertainty largely stalled what many expected to be a recovery year for commercial real estate. From shifting tax and trade policy to a higher-for-longer rate environment, the broader economic malaise left many in the sector hesitant to invest or transact.^1^

These themes are evident in members’ active investments, which reflects many of the challenges playing out across the broader CRE market. Elevated rates have weighed on valuations and slowed transaction activity, while refinancing hurdles and higher operating costs have tested (sponsors).^2^

Of course, challenges in recent vintages are familiar to most (CRE investors). The question now is what to expect from the market ahead.

Recent survey data suggests that confidence may be returning to the market.

In October, the (Fed delivered another 25-basis-point rate cut), its second of 2025. The market is predicting one more by year’s end.^3^ Economic policy uncertainty has fallen sharply since its April peak.^4^ And the fall has seen significant month-over-month surges in property listings.^5^

These developments are reflected in LightBox’s CRE Activity Index, which reached its highest level of the year in September, and in Deloitte’s annual investor survey, which found nearly 75 percent of respondents plan to increase their CRE allocations next year.^6^

It’s welcome news for investors eager for a more active market. But significant risks remain — and performance continues to vary widely by (asset class).

This report provides an overview of some macro and asset-level trends shaping CRE today. Then, we place those themes in the context of the more than 500 active real estate deals held in Crowd Street member portfolios.

II. Market Overview: Economic and Sector Trends

Quarterly economic data is usually released one to two months after the quarter ends, so these reports typically reflect conditions from the previous quarter, as is standard for this type of analysis.

Macro Statistics

Gross Domestic Product: GDP growth rebounded to 3.0% in Q2 after a 0.5% contraction in Q1. Full-year growth is projected at 1.7^%.^7^

Job Market: Hiring slowed sharply, with job gains averaging just 35,000 per month last quarter.^7^

Retail Performance: Sales rose 0.5% month over month in Q2 and 3.9% year over year in July.^8^

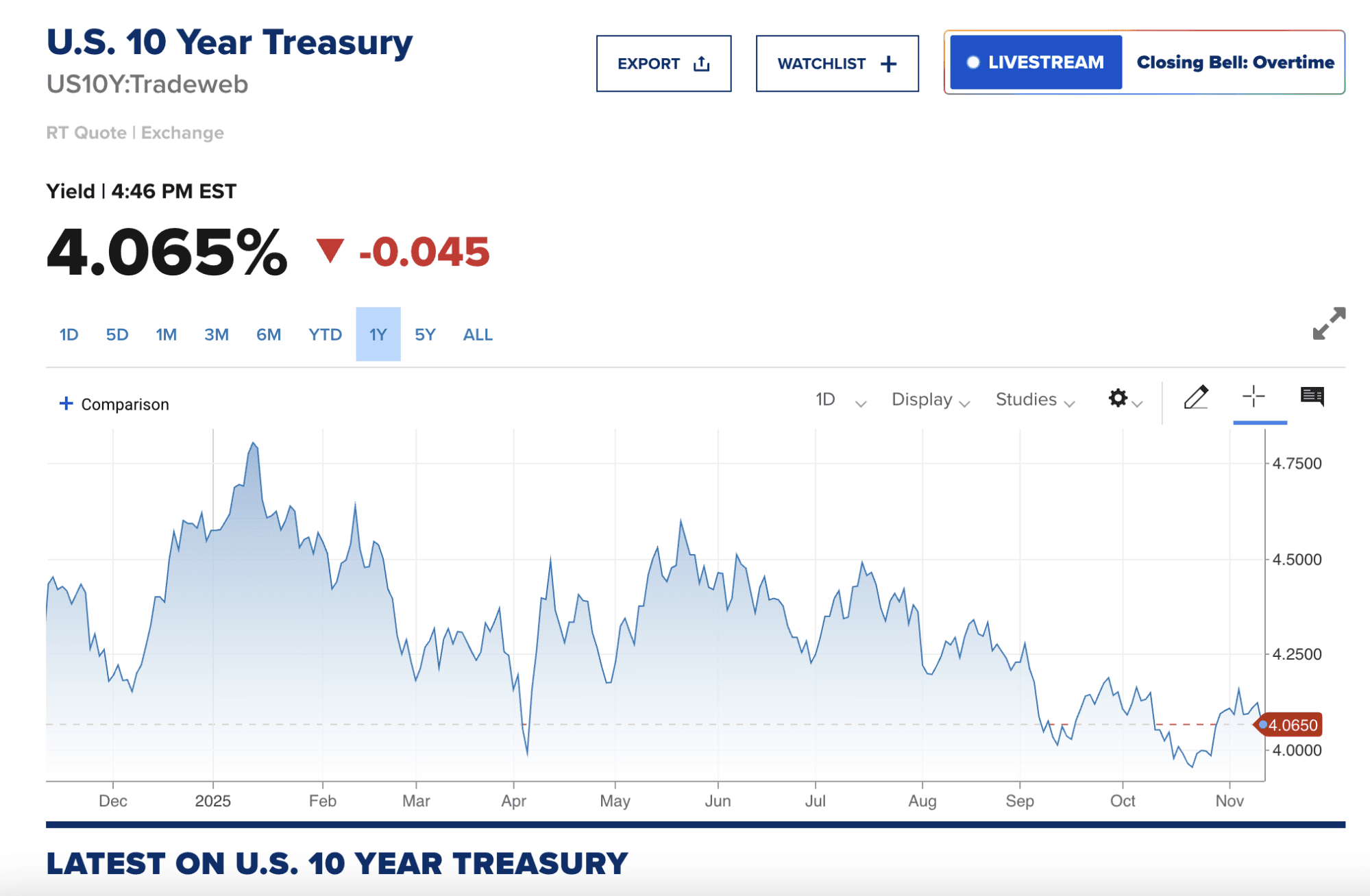

Treasury Yields: The 10-year yield fell to 4.068% as of November 12, down from roughly 4.7% in May.^9^

Rate Cuts: The Fed lowered rates by an additional 25 basis points at its October meeting, and markets expect one more cut before year’s end, according to the CME FedWatch Tool.^3^

Data as of November 12, 2025; graphic courtesy of CNBC.

Key Takeaways

Arguably, the biggest story of Q3 was the Fed’s long-awaited first rate cut of 2025. In October, the Fed announced an additional 25-basis-point reduction that lowered the federal funds rate to 3.75–4.00 percent.^10^ Though it’s tempting to see this as a clear tailwind for CRE, the reality is more nuanced.

A rate cut can certainly benefit some CRE participants, particularly those with floating-rate debt, such as construction loans, by easing borrowing costs. It can also help boost bank liquidity, potentially supporting more transaction activity.^11^

But most CRE fundamentals — like permanent loans, mortgages, and cap rates — are generally more closely tied to long-term yields, which move based on inflation expectations and growth outlooks, not the federal funds rate. The 10-year Treasury, for instance, remains the benchmark most strongly correlated with cap rates and property values.^12^

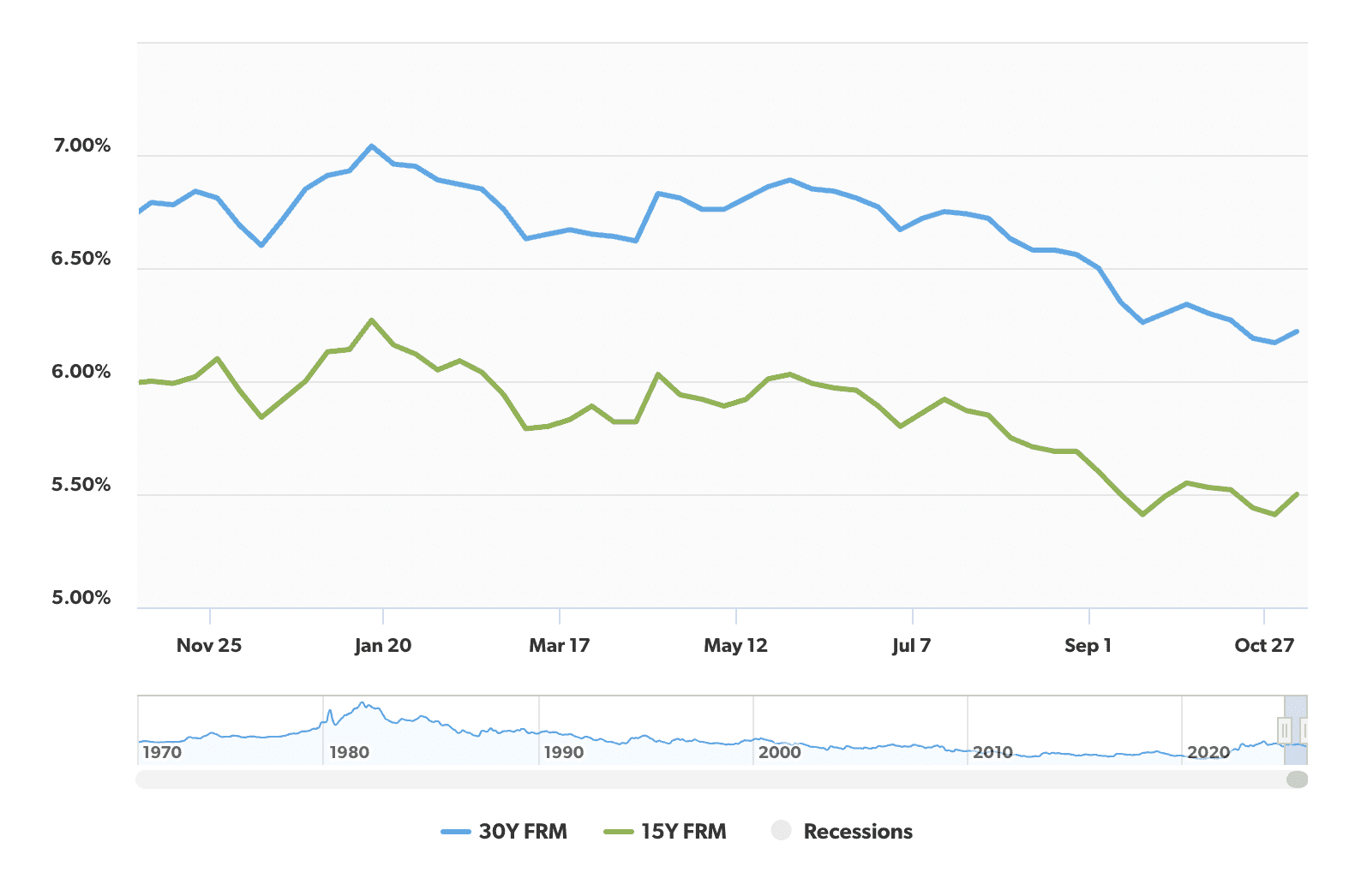

The good news: the 10-year Treasury has fallen too, hovering just above 4 percent after summer highs near 4.7 percent. Mortgage rates have also declined.^13^ These shifts are likely to have a greater impact on CRE markets than the Fed’s cuts.^14^

Mortgage rates over the past six months; data as of November 12; graphic courtesy of Freddie Mac.

CRE Market

Transaction Activity: Volume rose 13 percent year over year in Q2 when excluding entity-level transaction volume such as Blackstone’s $10 billion acquisition of AIR, which transacted in 2024.^15^ Early data from September points to the most active month of 2025 so far.^1^

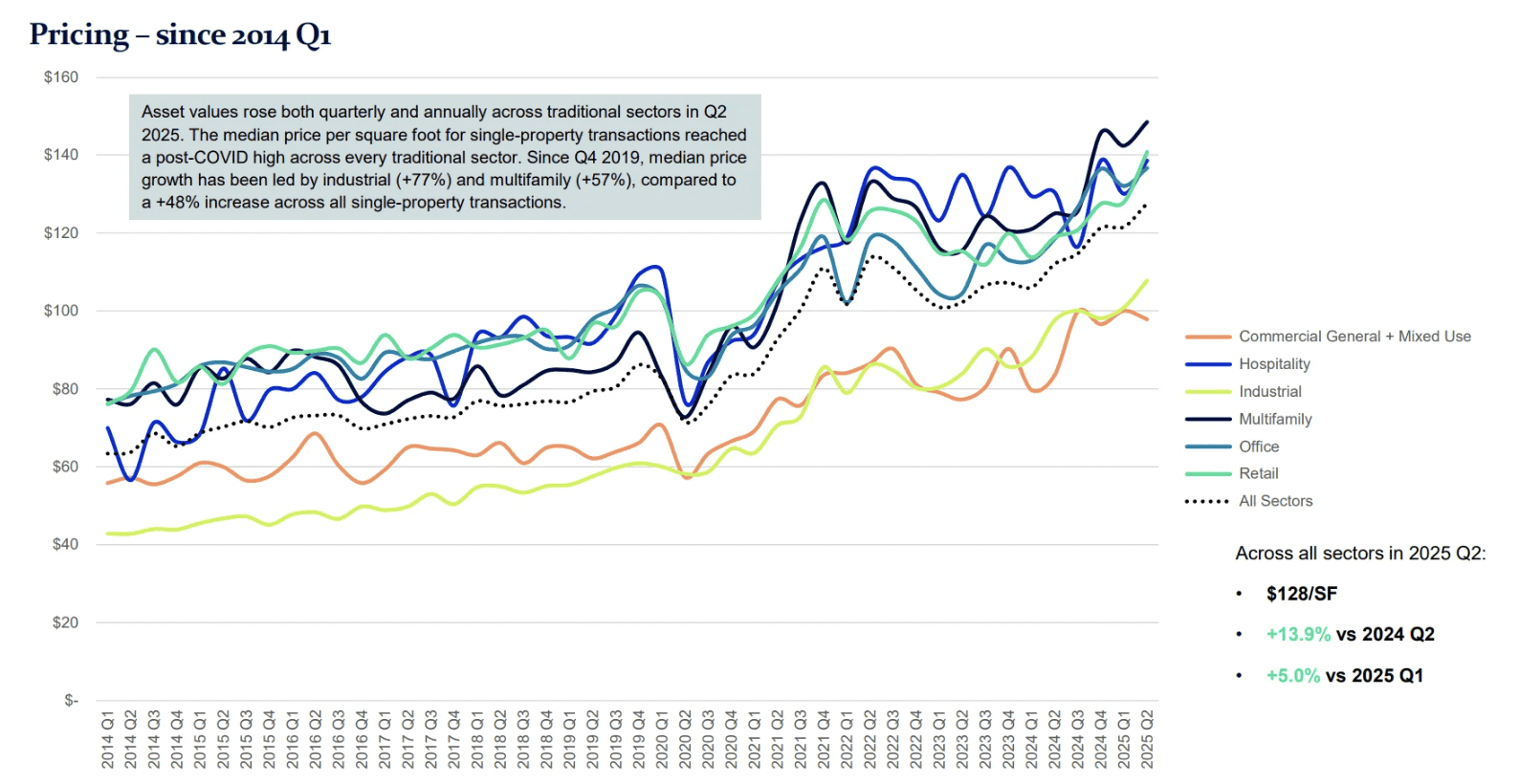

Pricing: The median price per square foot increased 5 percent quarter over quarter and 13.9 percent year over year.^16^

Building Size: The median building size traded grew across nearly all property types.^16^

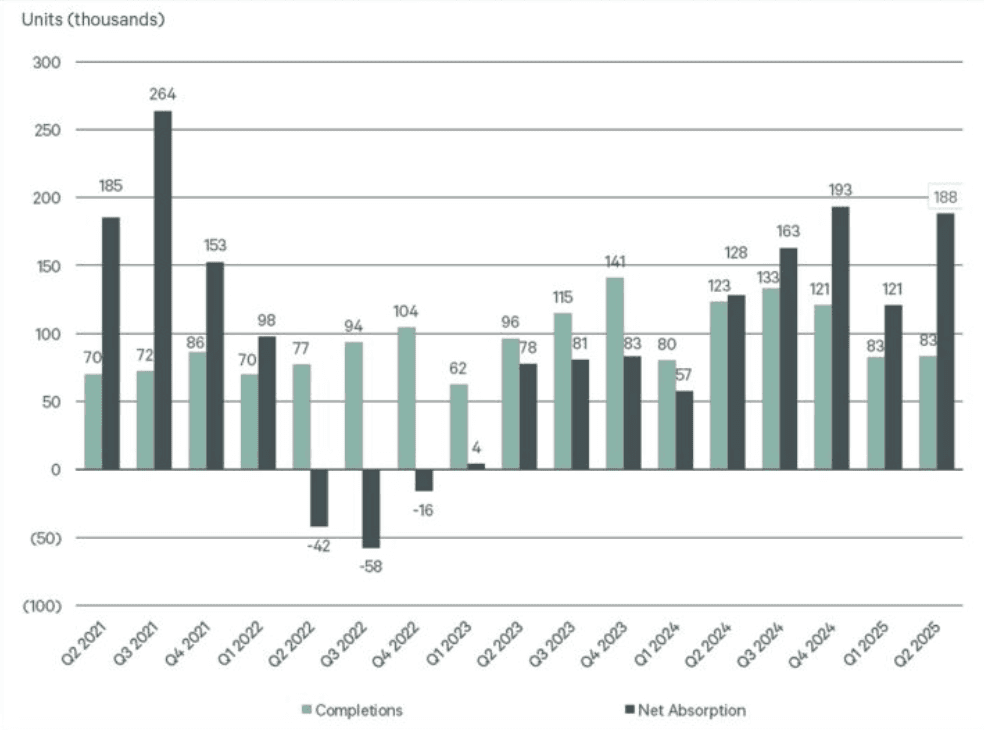

Absorption: Net absorption remains deeply negative.^17^

Key Takeaways

Broadly, the CRE market continues to send mixed signals. Buyer interest appears to be strengthening, with both transaction activity and pricing on the rise. This is driven in part by institutional capital gradually returning to the sector.^18^

Graphic courtesy of CRE Daily; data courtesy of Atlus Group.

At the same time, negative net absorption continues to weigh on valuations, a trend that’s likely to persist until the current oversupply is worked through.^17^

Performance varies widely by asset type, so sector-level data only tells part of the story. Let’s take a look at how each of the major asset classes have performed in recent months.

Asset Performance

Multifamily: A Supply-Demand Inflection Point

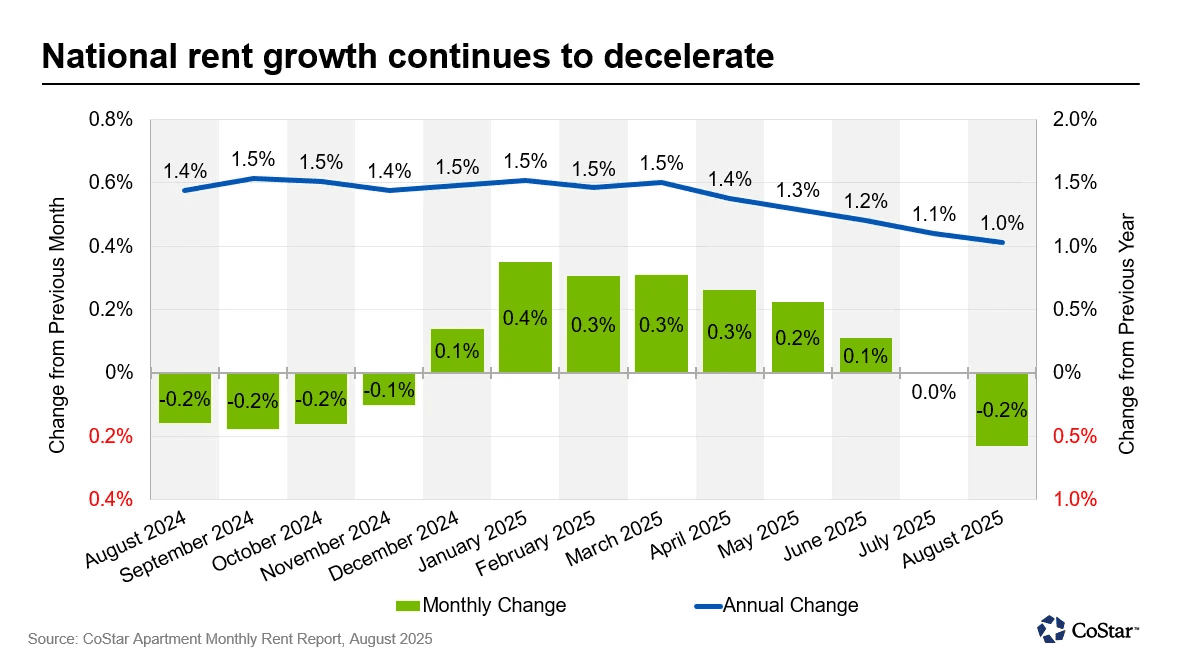

Multifamily fundamentals are beginning to rebalance as absorption finally outpaces deliveries for the first time since early 2025.^19^ Vacancy rates are tightening, new supply is falling sharply, and project starts have dropped to decade lows amid high capital costs and tighter lending. With national rent growth modest at around 1 percent year over year and expected to edge up by year-end, the sector appears to be approaching a supply-demand inflection point.^20^

Multifamily demand outpaces new supply; graphic courtesy of CBRE.

Industrial: Vacancy Pressures & Demand Headwinds

Industrial vacancies have climbed to 7.4 percent — the highest level in a decade — as new deliveries continue to outpace demand. Rent growth has slowed sharply amid weaker absorption, trade tensions, and a pullback in e-commerce activity. Smaller spaces are holding steady, but larger logistics facilities face slower lease-ups and oversupply.^21^

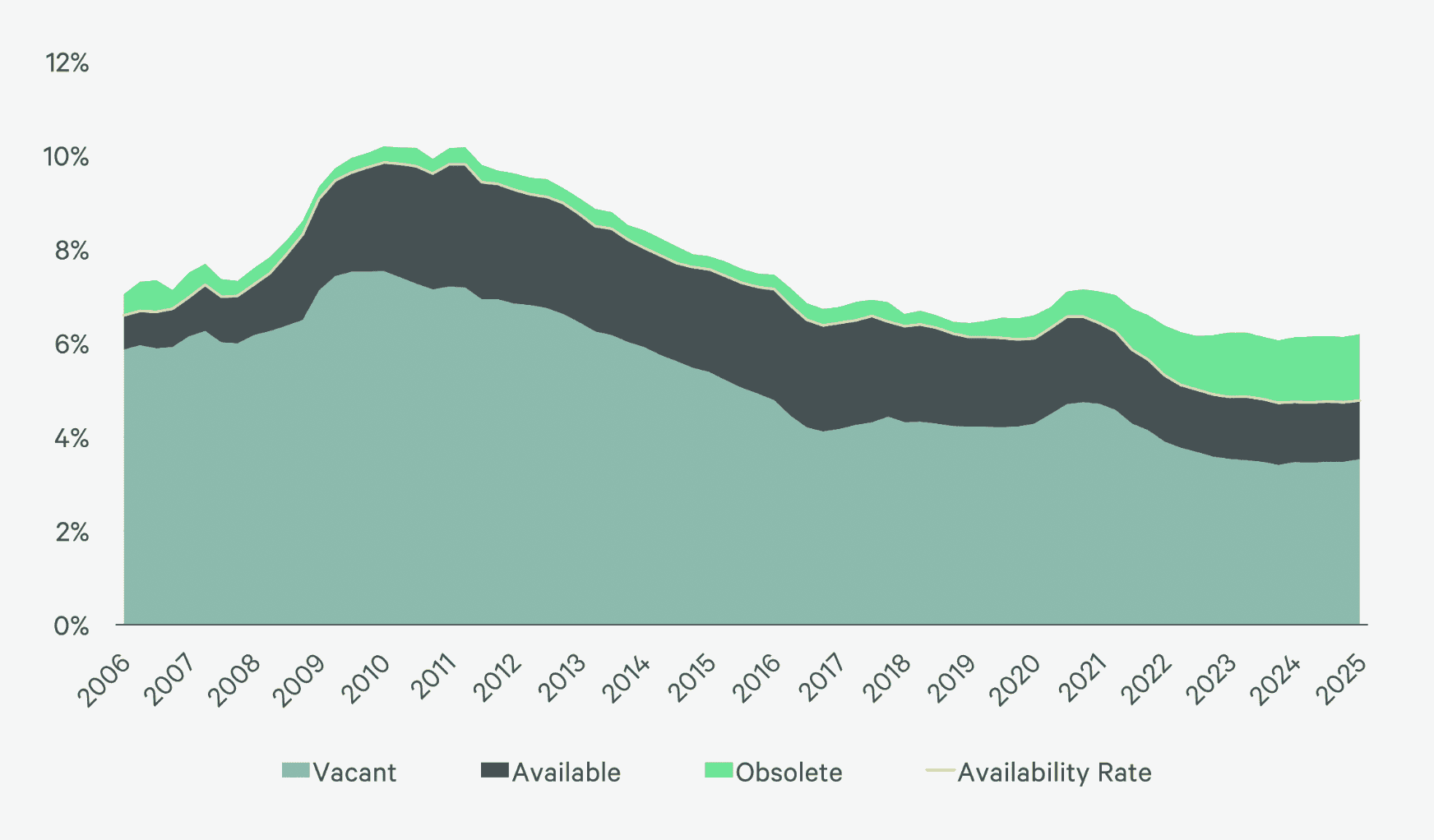

Retail: Recalibration & Resilience

Retail remains relatively resilient despite two consecutive quarters of negative absorption and lingering fallout from recent bankruptcies. Availability has risen, but strong backfill demand, faster lease-ups, and limited high-quality space continue to support the sector. Rent growth has eased slightly yet remains near multi-decade highs at 1.9 percent year over year.^22^

Retail vacancy rate, availability rate & percentage obsolete; graphic courtesy of CBRE.

Office: Fragmented Recovery & Elevated Vacancy

Office fundamentals remain weak, with overall vacancy at 19.0 percent and rent growth projected to stay below 1 percent through 2027. Deliveries have fallen to their lowest level in more than a decade, which may help stabilize select markets as new supply dries up. Top-tier buildings continue to outperform, while lower-quality assets face persistent pressure.^23^

Key Takeaways

One often hears the CRE market described in broad strokes, but as the dynamics above make clear, understanding it requires distinguishing between asset classes. Some sectors are gaining momentum, while others continue to face headwinds.

Multifamily and retail are showing encouraging signs — multifamily through tightening supply-demand dynamics and retail through relatively resilient leasing. At the same time, industrial and office remain constrained by oversupply and weaker demand.

For investors, that means selectivity may matter more than ever. In an uneven market, we observed that performance is increasingly driven primarily by quality, geography, and asset type rather than broad macro trends.

III. Portfolio Insights

The themes in active deals, previously offered through our platform, generally reflect what’s happening across the broader commercial real estate market.

Higher interest rates, rising costs, and limited liquidity continue to challenge both individual sponsors and large institutions. But there are also signs of progress: transaction activity is slowly improving and falling long-term yields could help ease some of the pressure on refinancing and valuations.^6^

Many 2021–22 vintages are under financial or operational stress, with refinancing hurdles, elevated loan balances, and cost overruns driving capital calls and recapitalizations. Still, sponsors are adjusting — working to find ways to manage through the cycle, preserve assets, and potentially position for recovery as rates begin to ease and market conditions gradually improve.^24^

Overall, currently active deals reflect a moment of recalibration shared by CRE investors across the market. Let’s take a closer look at how it’s playing out.

Operating Trends

Occupancy: Leasing activity is uneven — strong in coastal multifamily and top-tier office, weaker in industrial and high-supply multifamily markets (especially in parts of the Sun Belt).^25^ Concessions are rising in oversupplied areas.^26^

Rent Growth: Flat to modest across multifamily, office, and retail, limiting flexibility in underwriting and reducing the feasibility of new development.^27^

Cost Pressures: Insurance costs have doubled for many CRE owners,^28^ while property taxes and payrolls are exceeding budgets in some cases.^29^ Labor and materials inflation — partly driven by tariffs — remains a persistent headwind.^30^

Graphic courtesy of CBRE.

Capital Flows & Valuations

Valuations Depressed: Selling remains unattractive in many instances. Transaction volumes have picked up but are still well below pre-COVID averages, reflecting broad valuation markdowns.^2^

Portfolio Stress: 2021-22 vintages are experiencing the sharpest financial and operating pressure, reflecting the run-up in leverage and higher debt costs.^23^

Market Alignment: Broader valuation resets are mirrored in Crowd Street active deals.

Capital Calls

Investors are seeing more sponsors issue capital calls — why?

Development & Cost Overruns: Rising material and labor costs, delays caused by supply chain constraints, and challenges getting municipal approvals are squeezing project budgets.^29^

Ongoing Interest Rate Risks: Even with modest easing underway, borrowers with floating-rate loans face elevated costs. Many rate caps expire after one to two years, exposing them to rate resets.^31^

Debt & Market Conditions: Refinancing is becoming more difficult given the rising rate environment, while property values have depreciated, and oversupply and tenant concessions are adding pressure.^32^

Rising Operating Expenses: Insurance, taxes, payroll, and material costs are all climbing, putting additional strain on margins.^33^

Ultimately, these capital calls are meant to bridge funding gaps and extend hold periods until market conditions improve. As discussed here, many sponsors expect a recovery to take shape in 2026, and early data may support that outlook. Their goal is to carry projects through the current slowdown and into a more favorable environment for exits.

Realizations

Overall, sales remain muted amid the valuation pressures and headwinds outlined above, and when realizations do occur, outcomes are largely shaped by sector quality.

IV. Strategic Considerations

Two common questions Crowd Street hears from commercial real estate investors with allocations to current vintages are: (1) What’s driving extended hold periods? and (2) Why are business plans being revised?

Both themes are visible across Crowd Street active deals and throughout the global CRE market. While earlier sections touched on these dynamics, this final section takes a closer look at each in more detail.

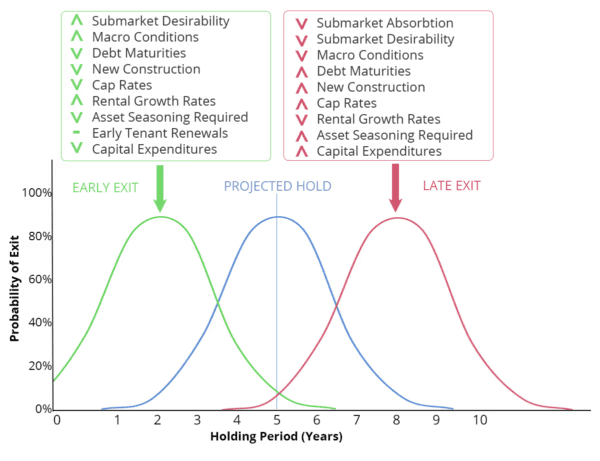

What’s driving extended hold periods?

As discussed, sales are widely viewed as unattractive in the current market. Higher interest rates have compressed property values, leaving many sellers unwilling to transact at discounted prices. And many buyers are cautious about underwriting lagging rent growth and elevated vacancy rates, further dampening deal activity.^2^

At the same time, optimism is building about the market ahead. The 10-year Treasury yield has eased, the Fed has begun a modest rate-cutting cycle, regulatory conditions are steadier, and supply-demand dynamics have improved across several asset classes — especially multifamily.^6^

As a result, many sponsors are extending hold periods to “wait out” the market. They prefer not to sell into discounted conditions in 2025 when they anticipate stronger pricing in 2026. Some are also using the extra time to pursue asset-level improvements — recapitalizations, operational upgrades, or refinancings — aimed at positioning properties for a potentially more transaction-friendly environment.^34^

Extended holds don’t guarantee stronger performance, but they reflect a strategic effort by many sponsors to protect value and prepare for potentially better market conditions ahead.

This chart is hypothetical and is for illustrative purposes only.

Generally speaking, sponsors are motivated to work to deliver optimal results for themselves and their investors, and that may translate into exiting a deal early or holding it longer than originally planned.

Why are business plans being revised?

Like extended holding periods, business plan revisions are becoming more common as sponsors adjust to a market that looks very different from the one they underwrote just a few years ago.

In some cases, revisions stem from recapitalizations or rescue capital: new equity injections that sit in a priority position in an effort to stabilize a project. While expensive, these deals can bridge short-term funding gaps created by cost overruns or debt maturity events, potentially helping sponsors preserve ownership and avoid distressed sales.^35^

Refinancing pressures are another major driver. As loans mature, higher rates and tighter lending terms often mean new financing requires significant principal paydowns. This often forces sponsors to rework pro formas, adjust cash flow projections, and extend hold periods in an effort to rebuild equity over time.^37^

Finally, operational realities are prompting on-the-ground changes. Insurance costs have in some cases doubled, property taxes and payrolls are exceeding budgets, and leasing incentives are eroding margins. To adapt, sponsors are cutting expenses where possible, pursuing creative re-tenanting strategies, or making targeted upgrades in an effort to improve occupancy and NOI.3^32^

In essence, these business plan revisions are usually adaptive measures with the goal of protecting value and keeping assets on track through an unusually volatile period. In general, sponsors’ goal is to emerge stronger when market conditions potentially normalize.

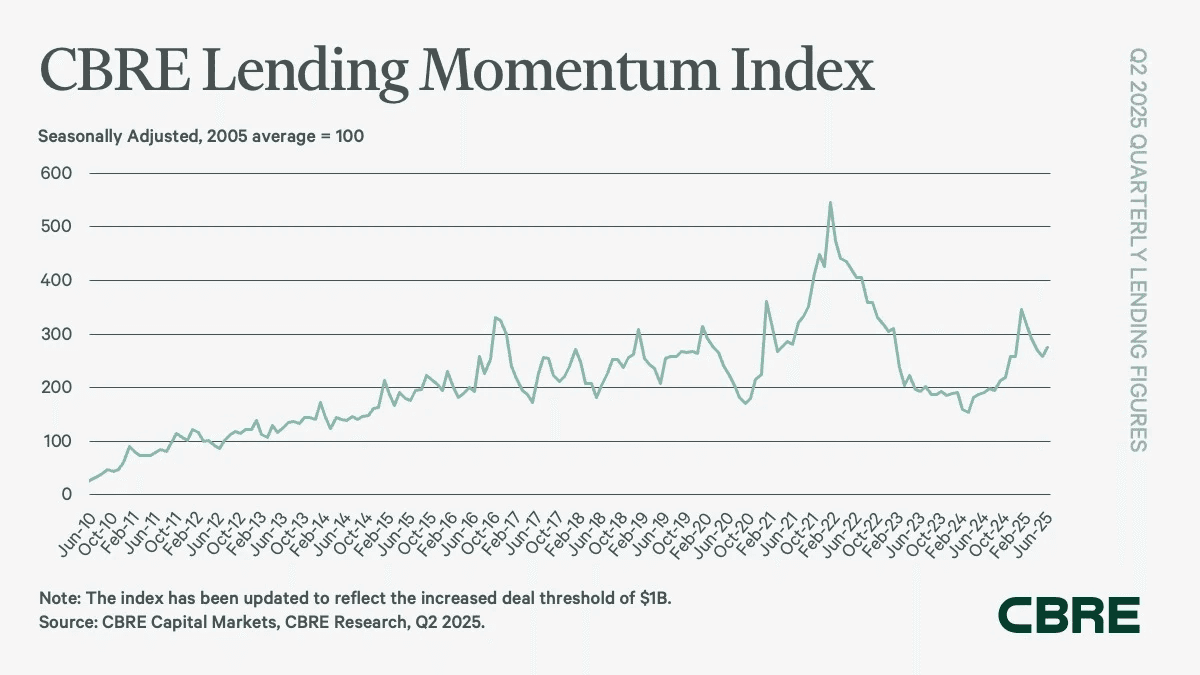

CRE lending activity remains subdued, underscoring the refinancing challenges driving many sponsors to revise business plans. Graphic courtesy of CBRE.

V. Conclusion

For most CRE investors — especially those active in the 2020–2021 vintages — this has been one of the most challenging periods in recent memory. That’s true not only of Crowd Street active deals but across the broader market, both in and outside the U.S.^30^

Still, there’s growing optimism among buyers, sellers, and investors that 2026 could mark the beginning of a new cycle. Principal Real Estate’s latest U.S. Commercial Real Estate Overview notes that the market has moved past its capital-markets shock and into a recovery phase, as pricing resets and visibility improve. Such conditions have historically preceded multi-year growth periods.^37^

That said, if this report reflects CRE stakeholders’ confidence in the future, it should also underscore the risks that remain today. Chief among them: the danger of viewing the market as monolithic when performance continues to vary sharply by asset type and geography. Selectivity, as discussed, remains a key lever for investors.^6^

For more insights from Crowd Street, visit our investor resources, where we regularly publish analysis on (commercial real estate), (private equity), (private credit), and other private market investments.