Leverage, or debt financing, is an important and even necessary part of most real estate deals. However, as the 2008 — 2009 real estate downturn highlighted, there are times when too much leverage on an asset can be a recipe for heavy losses. So, it is important for investors to understand leverage, the pros and cons of using it, what amount of leverage is prudent in a given situation and how it can influence the risk and reward of (real estate investments).

What is leverage?

Leverage refers to the total amount of debt financing on a property relative to its current market value. Loan-to-value ratio is another commonly used term when discussing leverage. However, Loan-to-value ratio refers to the amount of a single loan, such as a mortgage as a percentage of the value of a property. Leverage includes all of the different layers of debt in the capital stack, such as first and second mortgages and mezzanine financing. For example, a $10 million office building that has a $7 million mortgage and a $1 million mezzanine loan would carry 80% of total leverage.

What is the Upside of Leverage?

Real estate owners and developers often rely on leverage as a means to increase the potential return on an investment. The reason that leverage increases returns on a property is because the cost of debt financing, such as a bank loan, is usually cheaper than the unleveraged returns a property can generate. By inserting leverage, you can take the additional return from the leveraged portion of the project and apply it to the remaining equity to enhance leveraged returns. In simple terms, leverage allows investors to get substantially more bang for the buck.

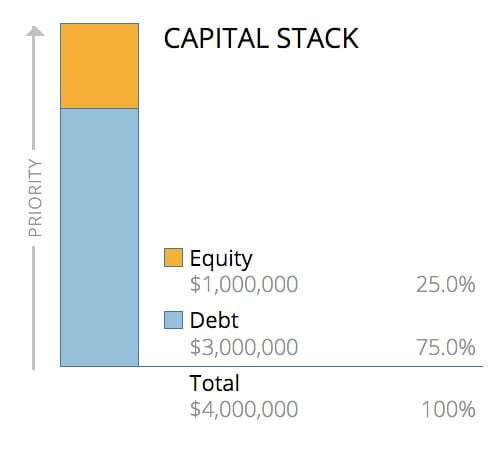

For example, one investor has $1 million in equity to invest and he decides to put 50% leverage on a property, which allows him to buy a $2 million retail building. A second investor has the same $1 million to invest, but she decides to use 75% leverage to buy a $4 million office building. From a capital stack perspective (for more details see my previous article, 'Understanding the Capital Stack') the two deals look like this:

In the first year, both properties appreciate by 10% and both investors decide to sell. Even though the two investors had the same amount of equity to start and both experienced the same percentage of property appreciation, the first investor makes a gross profit of $200,000 on the transaction while the second investor makes a gross profit of $400,000. This discrepancy in profits highlights the power of leverage in generating returns, assuming that things go well. The potential for this type of additional upside creates a strong incentive for investors to utilize higher leverage, sometimes as much as can be obtained.

How Much Leverage is Prudent?

In some cases, higher leverage can translate to higher risk. For example, there were plenty of three to five-year loans issued from 2005 to 2007, just prior to the recession at high leverage amounts of 85% to 90% of acquisition value. Adding to that risk is the fact that those loans were based off of what we now know were peak property values.

So, when the market shifted and property values dropped precipitously in 2008 to 2009, those borrowers found themselves underwater in the properties right at the point their debt matured. Similar to what happened in the housing market, certain borrowers found themselves in predicaments where the outstanding mortgage balances were higher than what the properties were now worth. When confronted with these situations, the only way to retain the assets was to de-leverage them or place new smaller mortgages on the properties (and even this was nearly impossible given the illiquidity at that time) and pay off the balance of the existing mortgages with newly infused equity. Tragically, the solution for many owners was to hand the keys back to the bank and walk away from debt-burdened properties.

While the overuse of leverage was the culprit of many failed deals during the financial crisis, the risk of high leverage can be mitigated through certainty of execution. For example, if a sponsor has a building that is fully leased to a stellar credit tenant such as Amazon on a long-term lease, it is reasonable to place a high level of leverage on such a property knowing that Amazon would have to go out of business before it stopped paying rent. In contrast, if a sponsor has a dozen tenants in a building, all of which are small mom and pop businesses on short-term leases, the safer play is to be more conservative on leverage knowing that the exposure to future vacancy, and hence lower income from the property, is remarkably greater.

Investors can analyze leverage as another metric to gauge the risk versus potential returns of (real estate projects) when making investment decisions. For example, when comparing one deal with a 16% Internal Rate of Return or 'IRR' and low leverage with and another deal that targets a 19% IRR but with high leverage, the lower IRR deal may actually be more favorable because the additional 300 basis points difference in targeted IRR may not adequately compensate the investor for the higher financing risk. This is what is referred to as 'risk-adjusted returns'.

The Use of Leverage in the Current Cycle

While the downturn in the commercial real estate market in 2008 and 2009 produced some harsh lessons on leverage for certain owners, it has also spawned opportunities for investors in the current cycle. The subsequent deleveraging of commercial real estate in the aftermath of the downturn has created a need for higher percentages of equity in capital formation. This shift to the use of greater amounts of equity has helped propel growth for (real estate investing platforms) such as Crowd Street. Despite the post-recession recovery, some lenders remain relatively conservative and, as a result, lower levels of leverage are more the norm, perhaps for good reason. That has created opportunities for real estate investors to fill that financing gap via both equity and debt real estate investments.

Getting Started with CRE Investing Has Never Been Easier

Crowd Street offers both debt and equity investment offerings on the Crowd Street platform. Sign up for a free account and view our current deals.